“`html

Smart Ways to Handle Debt: Discover the Minimum Amount Required to File Chapter 7 in 2025

Handling debt can be overwhelming, especially when you’re considering drastic measures like chapter 7 bankruptcy. Understanding the minimum debt amount required to file for this type of bankruptcy in 2025 is crucial for many people facing financial hardship. In this article, we will explore the debt limits for chapter 7, the eligibility criteria, the filing process, and what you can expect in terms of outcomes and impacts on your credit score.

Understanding Eligibility for Chapter 7 Bankruptcy

Before filing for chapter 7 bankruptcy, it is essential to understand the bankruptcy filing requirements. Typically, you must pass the means test, which evaluates your income and expenses to determine eligibility. The means test considers your household income compared to the median income of a similar household in your state. If your income is below the median, you’re automatically eligible to file; if it’s above, further calculations are necessary.

Debt Limits and the Means Test

As of 2025, the debt amount chapter 7 can vary based on state statutes, but an individual’s unsecured debt such as credit cards and medical bills will primarily influence eligibility. The threshold for unsecured debt is significant; exceeding this can see you shifted towards a different bankruptcy chapter, such as chapter 13. The credit counseling requirements, mandated prior to filing, can provide insights into managing your debts more effectively, as well as clarify your position regarding debts that qualify for chapter 7.

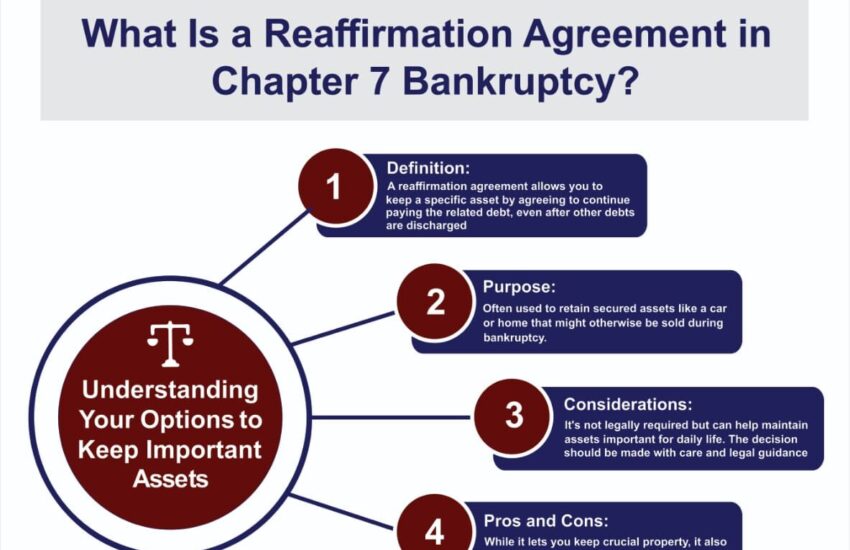

Types of Debt That Qualify for Chapter 7

Not all debts can be discharged under chapter 7 bankruptcy. Common debts that typically qualify include unsecured debts, such as credit card balances and medical bills. However, specific obligations like student loans, child support, and tax debts are usually non-dischargeable. Familiarizing yourself with bankruptcy dischargeable debts can aid in constructing a planned approach to your financial recovery.

Filing Process for Chapter 7 Bankruptcy

The bankruptcy process chapter 7 begins with gathering financial documents such as income statements and details of debts and assets. It’s imperative to accurately fill out the chapter 7 bankruptcy forms and file them with your local bankruptcy court. Once your case is filed, an automatic stay goes into effect, offering immediate relief from creditor actions while your bankruptcy is processed.

Document Preparation and Filing Fees

Preparing for your chapter 7 case involves a detailed financial assessment, including documentation on assets chapter 7 bankruptcy. Filing fees may apply, typically ranging from $300-$400, along with the documents for filing your case. Consider setting aside funds to cover these ongoing fees and other costs, as the completion of the bankruptcy process can take several months.

The Timeline for Chapter 7 Captured

Understanding the chapter 7 timeline is essential for those preparing to file. Typically, the process takes about 3 to 6 months from the initial filing to discharge. During this period, a court-appointed trustee evaluates your financial situation and may initiate liquidation of any non-exempt assets. Knowing what to expect during this timeline can alleviate the worries that come with bankruptcy proceedings.

Consequences of Filing Chapter 7

If you decide to file for chapter 7 bankruptcy, understanding the potential impact on your credit score is crucial. Generally, you can expect a significant drop in your credit standing, lasting for up to 10 years. However, responsible financial behavior after filing chapter 7 can expedite your credit recovery and foster future opportunities.

Emotional and Financial Recovery Post-Bankruptcy

The emotional toll of filing for bankruptcy can be considerable. Many individuals experience feelings of shame or defeat; however, it’s vital to focus on long-term financial management after bankruptcy. Engaging with a financial advisor or considering debt management strategies can help you rebuild your finances and improve your financial literacy.

Credit Recovery Post-Bankruptcy

Rebuilding your credit score after chapter 7 bankruptcy is possible through responsible management practices. Begin by acquiring a secured credit card and ensuring timely payments. Additionally, actively monitoring your credit report for errors and ensuring old negative marks are removed over time can enhance your credit profile.

Key Takeaways

- Understand the debt limits for chapter 7 as they can affect your eligibility.

- Be proactive in preparing for the bankruptcy process by collecting necessary documents.

- Anticipate the long-term impacts on your credit score and engage in practices to mitigate negative effects post-bankruptcy.

- Seek professional assistance to navigate the complexities of bankruptcy laws.

FAQ

1. What is the minimum debt amount required to file for Chapter 7 in 2025?

While there is no official minimum debt amount specified, generally, individuals with significant unsecured debt chapter 7 must typically evaluate any debts within a realistic range that signifies potential hardship. Each case is reviewed individually, taking into account available income and assets.

2. How does Chapter 7 bankruptcy affect my credit score?

Filing for chapter 7 bankruptcy may lower your credit score significantly, lasting for up to 10 years on your report. Employment, housing, and future credit could all be affected during this time, making it crucial to focus on rebuilding your credit responsibly afterwards.

3. What assets can I keep when I file Chapter 7?

Under bankruptcy exemptions, you may retain certain essential assets, including your primary vehicle, home equity up to a specified limit, and some personal belongings. Understanding these exemptions chapter 7 bankruptcy is vital to maximizing what you can retain while discharging debts.

4. Can I file for Chapter 7 if I have a job?

Yes, many individuals working full-time qualify for chapter 7 bankruptcy, largely contingent on their income level and overall debt. The means test chapter 7 will assess your financial situation and determine your eligibility.

5. Will I need an attorney to file Chapter 7?

While it is possible to file chapter 7 without legal assistance, retaining a bankruptcy lawyer can significantly streamline the process and help navigate the complexities of the bankruptcy court system, potentially safeguarding your interests and investments.

“`